We've worked on loyalty initiatives across insurance and adjacent industries, and one pattern emerges again and again: engagement often rises when incentives or reward mechanics are introduced, but long-term retention rarely changes in a meaningful way.

The issue isn't that customers dislike rewards. It's that loyalty in insurance is shaped far less by programs than by the quality of a few critical moments in the journey: onboarding, policy changes, documentation, and above all, claims.

By nature, insurance tends to fade into the background of daily life. When things are going well, customers rarely think about risk, policies, or coverage. Most insurance apps are opened only 2–3 times a year, usually to file a claim or check something near renewal. That invisibility isn't necessarily a problem, it reflects the role insurance is meant to play.

The challenge begins when invisibility turns into absence. Without meaningful interactions throughout the year, there's no relationship. And without a relationship, renewal becomes purely rational: price!

This article explores how insurers can move beyond loyalty as a promotional layer and treat it as a structural element of the customer experience, designing digital journeys that create clarity, certainty, and trust long before renewal arrives.

Retention is no longer defensive, it is economic

The economics of insurance make this shift unavoidable. Acquisition costs continue to rise, competition intensifies, and customers are more willing than ever to switch providers. At the same time, the majority of revenue in most insurance portfolios comes from existing customers. Even small improvements in retention can generate disproportionate gains in profitability.

Loyal customers do more than renew. They expand coverage. They consolidate policies. They recommend. And they are typically less sensitive to price fluctuations because their decision is not purely transactional, it is relational.

Treating loyalty as a promotional tool underestimates its financial impact. In today’s market, retention is not simply about preventing churn. It is about protecting margin and strengthening lifetime value.

A 5% retention improvement boosts profits 25-95%

In practical terms, this means retention should be framed with the same rigor as acquisition. Instead of measuring only policy counts and lapse rates, insurers can track metrics such as time to certainty in claims, task completion rates in digital journeys, or the share of self-service interactions that end without escalation. These indicators reveal where trust is being strengthened or eroded long before renewal shows it in the numbers.

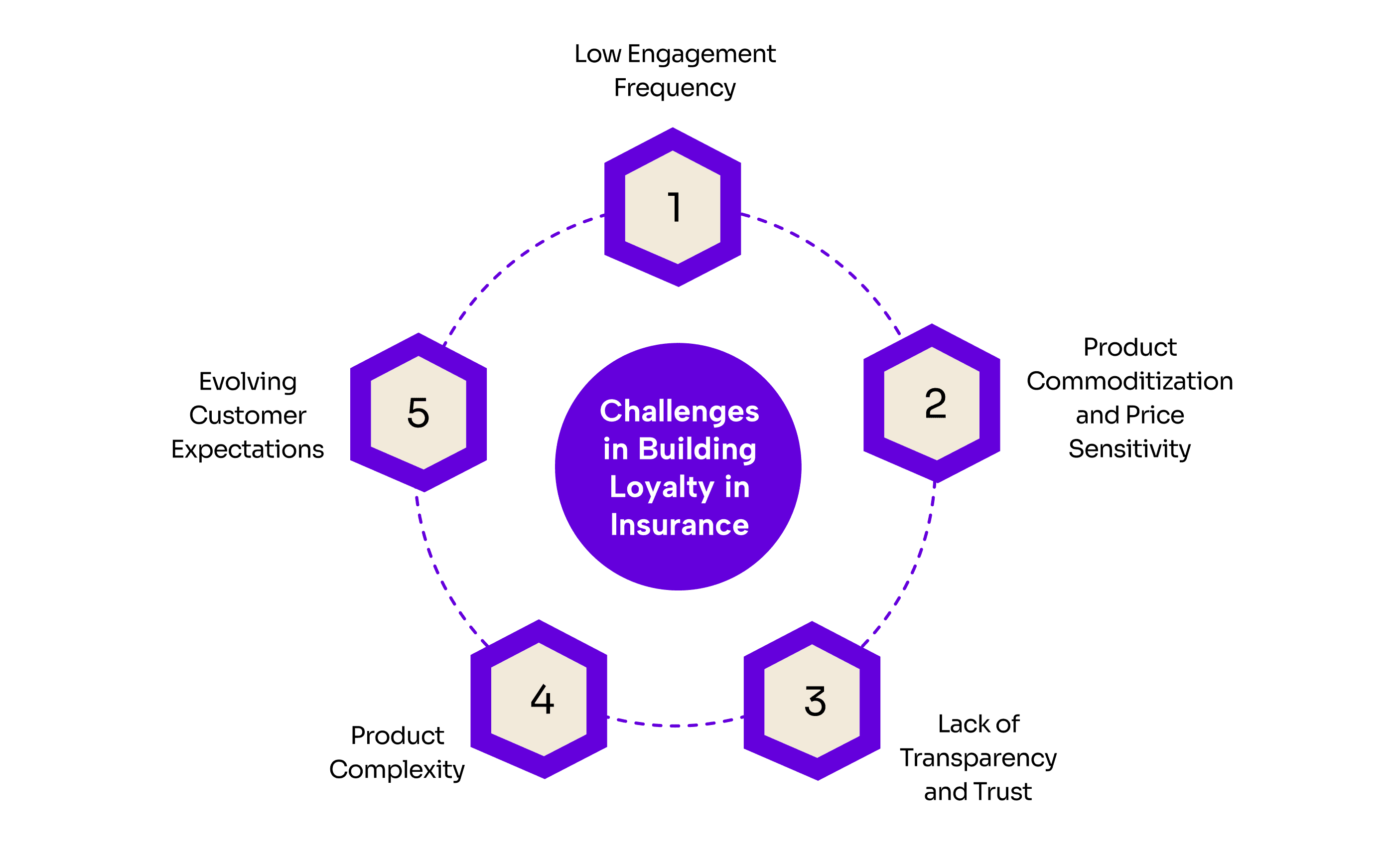

Why traditional loyalty models fall short

Many loyalty initiatives in insurance still rely on transactional mechanics: point accumulation, generic reward catalogs, renewal discounts. These tools may boost short-term engagement, but they rarely create long-term attachment.

The reason is simple: loyalty in insurance isn’t built through campaigns, it’s built through moments.

When those experiences are slow, unclear, or unnecessarily complex, trust erodes. Customers might not complain right away, but friction accumulates. And when renewal arrives, the emotional connection is weak, and price wins.

Often, that friction isn’t just procedural, it’s cognitive. Customers struggle to fully understand their coverage, limits, or what their policy actually protects. Clear, contextual explanations can make a decisive difference. When people feel confident in what they have and how it works, the relationship strengthens, and price matters less.

No reward program can make up for a fragmented experience. Loyalty isn’t an extra layer added on top of the customer journey, it’s the result of how that journey is designed.

The moments that truly shape loyalty

Across the industry, three structural factors consistently influence retention.

First, time to certainty. During a claim, customers want clarity as much as resolution. Reducing delays, eliminating repetitive manual steps, and communicating progress transparently all strengthen confidence. Even small gains in claims efficiency can significantly improve renewal rates.

Second, contextual communication. Loyalty does not grow through frequency alone. It grows through relevance. Explaining premium changes before renewal, anticipating required actions, and using the channels customers actually prefer turns communication from noise into value.

Contextual communication also means helping customers understand whether their coverage still matches their current needs. As life circumstances evolve (a new home, a growing family, a different risk profile), protection should evolve accordingly. Proactive explanations and recommendations position the insurer not only as a service provider, but also as a long-term advisor supporting customers through different stages of their lives.

Third, the balance between automation and human touch. Digital tools should remove friction, enabling fast quotes, seamless uploads, and real-time status updates, but they should not eliminate empathy where it matters most. In high-stakes interactions, human reassurance remains essential to trust.

For insurers looking to act on these three factors, the starting point is often surprisingly modest. Mapping one or two high-impact journeys, typically claims and onboarding, and running structured usability tests with real customers can uncover friction that internal teams no longer see. Small design changes, like clearer status messages, simpler document requests, or tailored explanations of coverage, frequently deliver outsized gains in satisfaction and retention.

When these elements align, loyalty becomes structural rather than promotional.

From points programs to relationship architecture

Redefining loyalty means shifting from incentive thinking to experience thinking.

Instead of asking, “How do we increase engagement with our program?”, insurers need to ask, “How do we design meaningful interactions throughout the year?”

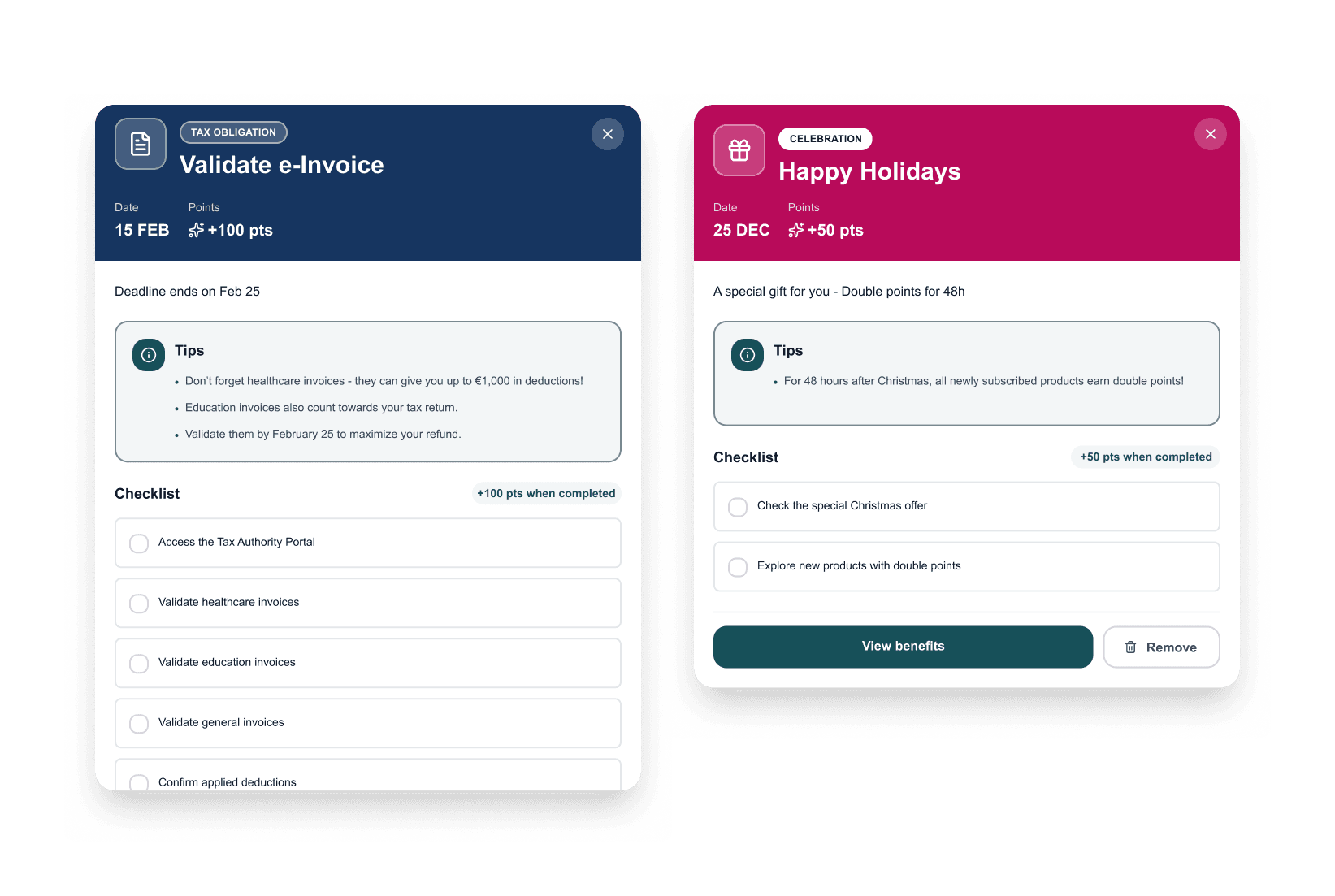

That requires mapping end-to-end journeys, identifying invisible friction points, and embedding relevance into digital touchpoints. This can translate into simple but meaningful capabilities, such as:

- Annual coverage check-ups that help customers review whether their protection still fits their life situation

- Contextual nudges when life events might affect their coverage

- Clear explanations of what is and isn’t covered in common scenarios

- Guided claims flows that adapt to the situation instead of forcing every case into the same template

These are not campaigns in the traditional sense, they are recurring, embedded interactions that quietly reinforce the value of staying.

By contrast, many loyalty apps still focus on generic content and undifferentiated offers that could come from any provider. When everything looks and feels interchangeable, customers naturally default to price as the main decision driver. Relationship architecture is about making it harder for competitors to replicate the experience, not just the offer.

For many customers, the app becomes the primary place where their relationship with the insurer is experienced. If it functions only as a service channel, engagement remains purely functional. But when the app becomes a space of clarity, guidance, and support, the dynamic changes.

Customers return not because they are reminded to, but because the interaction serves a purpose. The app becomes a place where they understand their coverage, receive relevant recommendations, and feel supported in their decisions.

In that context, price becomes one factor among many, not the only one.

Building loyalty by design

At Mediaweb, we see loyalty as a consequence of intentional digital experience design.

We work with insurers to analyze critical journeys, uncover friction that weakens retention, and redesign digital interactions with long-term relationship value in mind. This often involves combining qualitative insights (interviews, usability tests, service blueprints) with quantitative evidence from analytics and operational data. By examining drop-off points, repeat contacts, and common error patterns, we help teams prioritize which moments to redesign first, and which changes will most likely move the needle on both experience and retention.

Through strategic UX thinking, scalable front-end architecture, and hands-on implementation, we transform operational touchpoints into moments of confidence.

We don't treat loyalty as a standalone program, but as a system of relevance embedded into the experience

A strategic shift

We opened with a pattern we see consistently in insurance loyalty initiatives: programs boost engagement, but rarely move the retention needle. That's usually a sign the problem isn't the program, it's the experience around it.

If loyalty still lives primarily under marketing in your organization, it may be time to rethink its role. In insurance, loyalty isn't a campaign or renewal discount. It's the structure that determines whether customers see you as a provider or a partner.

In a market where switching has never been easier, that distinction separates leaders from price competitors.

If this is relevant for your organization and you would like to explore it further, we’ve worked with multiple insurers facing similar challenges. We can help identify where experience improvements will have the greatest impact on retention and help take your digital journeys to the next level.

Why do traditional loyalty programs fail to improve retention in insurance?

Traditional loyalty programs rely on transactional mechanics like points and generic rewards, but they can't compensate for fragmented experiences or friction in critical moments like claims or onboarding.

What moments in the customer journey most impact insurance loyalty?

The three most critical moments are claims processing (time to certainty), policy changes and documentation, and onboarding, as these interactions either build or erode trust.

How often do customers typically interact with their insurance apps?

Most insurance apps are opened only 2–3 times per year, usually to file a claim or check something near renewal, reflecting insurance's naturally low-visibility role in daily life.

Why does price become the main factor at renewal for many customers?

Without meaningful interactions throughout the year, there's no relationship, so renewal becomes purely rational and price-driven rather than relational.

What is the financial impact of improving customer retention in insurance?

A 5% improvement in retention can boost profits by 25-95%, as loyal customers expand coverage, consolidate policies, and are less price-sensitive.

How can insurers create meaningful interactions throughout the year?

By designing recurring, embedded interactions like annual coverage check-ups, contextual nudges for life events, clear coverage explanations, and guided claims flows that adapt to each situation.

Should insurance loyalty be treated as a marketing function?

No, loyalty should be treated as a structural element of customer experience and framed with the same rigor as acquisition, not as a promotional tool or standalone program.